The Great Permian Parlay: PXD | DoublePoint

“You don’t want to do an extension or fringe, you have to be in the areas with truly low break-evens” - Cody Campbell (DoubleEagle | DoublePoint)

Editor’s Note: **If you enjoy this newsletter - do us a favor, forward it to a colleague** -

Transaction Notes:

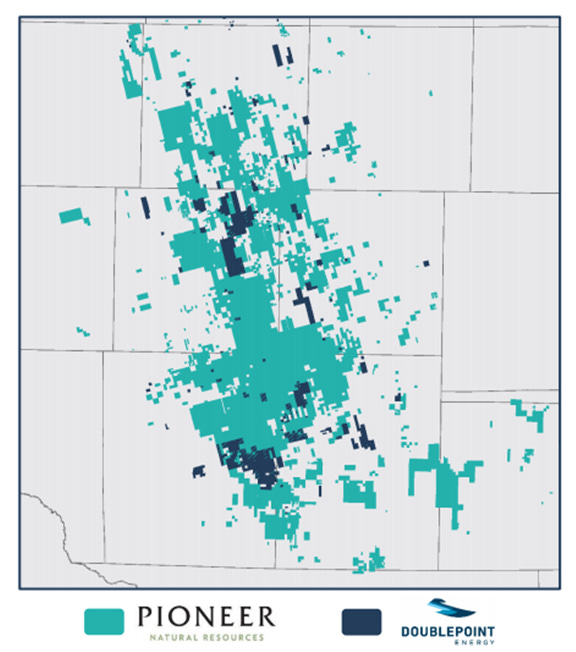

Pioneer | DoublePoint Presentation

A $6.4BN PARLAY.

The long Easter weekend provided cover for one of the larger recent Permian deals - the Pioneer acquisition of DoublePoint.

DoublePoint will receive:

~11% of Pioneer’s equity

$1BN in cash

Pioneer will receive:

~100,000 boepd (at close)

~1,200 core locations

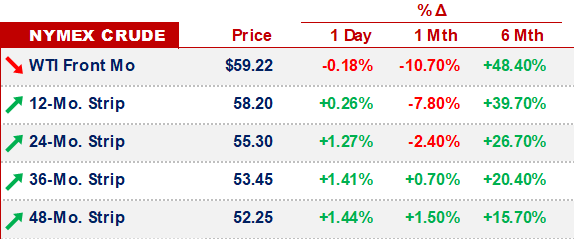

Relative to recent Permian transactions, the deal looks expensive.

However, those transactions were executed at a lower strip; with higher prices, we could understand a valuation that’s ~double.

That said, this deal was expensive, even on that basis:

HUSTLE & GAMBLE.

There’s a couple noteworthy pieces to this story.

The Campbell & Sellers / DoubleEagle acreage acquisition machine has been incredibly effective at scale (in ‘17, they sold ~71k acres to Parsley for $2.8BN).

It appears that the duo’s operation has been better - at acquiring top Midland basin acreage - than anyone else.

This time around, they had to do more (drilling) to prove out the acreage.

In 2020 of all years…

Scaling production in ‘20 was a gamble that - in the simplest terms - bet on oil prices mean-reverting.

DoublePoint increased rig-count at a time when almost all of their competitors cut rig-counts by half or more.

Doing so, DP committed to drilling wells at a negative NPV.

That’s a leveraged bet on WTI - like buying out-of-the-money calls on oil futures.

On top of that bet, the wells had to work.

And they did:

And - somehow - DoublePoint financed this bet with debt.

They drew-down on commitments to drill these wells, and then they re-fi’d those commitments with a private placement.

An acreage bet

A drilling bet

And a financing bet

All three paid out - for a $6.4BN parlay -

OTHER NEWS.

On Iran oil exports

India’s energy minister on net-zero targets

An interesting take on Netflix & Europe

Even the sell-side thinks the PXD/DP deal is expensive

That’s it for this week - congrats to Baylor - catch y’all next Tuesday -