Monetary Vaccination

“We Couldn't Just Sit Back & Do Nothing” - Mario Draghi

MACRO.

There’s 2x headlines going into the weekend:

Regulators & policymakers around the world are nervous (and rightfully so), echoing Mario Draghi’s bias-for-action attitude from the ‘11 Euro-Debt-Crisis.

The consensus takeaway from ‘08 & ‘11 was that preemptive action was much better than inaction (e.g. Greek bailout vs watching AIG go-under).

If you do nothing else, check up Central Bankers & OPEC+ today -

OPEC+.

Saudi wants oil production cuts from OPEC+Russia.

Most of the rest of OPEC wants Saudi to cut production, while they cheat & keep production at current levels.

And Russia… they smell blood.

The men who run Russia derived their power from 2x historical events:

The Fall of the Soviet Union

The Subsequent Privatization of Soviet State Assets

**for them, destabilization is spelled “de$tabili$ation”**

The coronavirus stands a chance to wreck economies around the world.

That pressure, compounded with lower oil revenues for OPEC member states will put a serious strain on their economies.

For Russia this is a heads-I-win, tails-you-lose opportunity.

Worst-case for Russia: lower oil revenue coupled with a strong geopolitical negotiating power

Best-case: Russia is able to take financial positions in key sectors of these strained economies

Russia’s currently running this playbook in Venezuela - Maduro is under pressure to privatize state oil assets.

From the 90s, the Russian Oligarchy knows that the lucrative play is long-term play.

When OPEC makes its production cut announcement, we don’t expect that the Russians will have played ball -

THE VIRUS.

Central Bankers fired their shots & cut rates.

They don’t have many bullets left.

With historically low rates, we expect Tier 1 Residential Real Estate (in the Western World) & un-leveraged Software Equities to benefit significantly.

But that doesn’t help the rest of the global economy.

A former Fed Governor spoke earlier this week, and we agree with his take:

“The Fed can't cure the virus.

If you have a breakdown of global supply chains, that's a supply issue that the Fed can't directly address.

During the financial crisis in '08/09, there was a dollar liquidity shortage - everyone wanted dollar liquidity. The Fed could do something directly about that ['08/'09]...

...it [this Fed rate cute] can't get at the fundamental of the problems of the virus” - Randy Kroszner, former Fed Governor

All that said, we don’t fault the Central Bankers for trying.

Politics aside, we don’t think their actions made anything too much worse (although urban rents will rise - w/ the urban poor feeling the most pain).

And they quickly & transparently did what they could.

Which more than can be said about many other responses to the virus -

SHALE.

BAML & Bloomberg published a few interesting graphics this week.

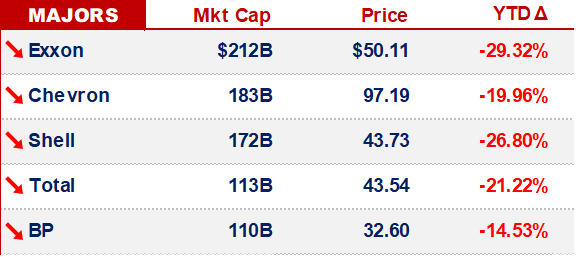

Bloomberg’s graph gives a whole new - almost cannibalistic - meaning to the saying “Eat What You Kill”:

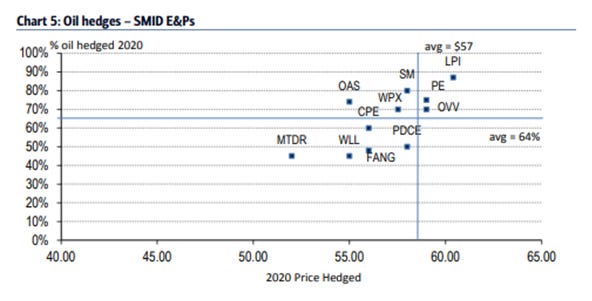

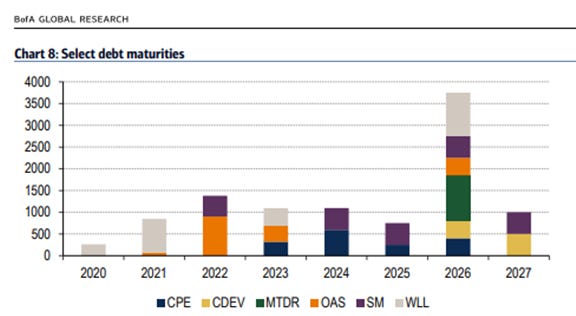

BAML highlighted that - for some E&Ps, if trouble comes - it may not be until ‘21:

SMID E&Ps aside, Exxon’s analyst day was covered by an anonymous Twitter Acct - we won’t recreate the thread, but we do recommend giving it a quick look.

[For those who aren’t familiar - many financial analysts cannot publicly comment on securities & use Twitter to publish notes to the public]

The main highlight is the inconsistency in 5+yr forecasts, YoY.

On account of both good & bad news.

In any case - one thing is consistent - no one’s been hitting forecasts -

OTHER NEWS.

Berkshire Hathaway bails on the Saguenay LNG project

Trafi & Vitol are now in the LNG derivatives business

Extraction & Montage reported

The human element of US Shale

Bookmakers now have Biden safely clear of Bernie

That’s it for this week - hope y’all enjoy the weekend - stay well -