Hwang'd

“The only reason oil is higher is because Saudi has defended the price by cutting production. Demand hasn't come back. So the thesis we're putting on the table is if demand does recover as most people are expecting in a post-COVID world” - Doug Leggate, BAML

BILL HWANG.

There are two new verb phrases on Wall Street:

“Going-Bill-Hwang”: taking a large, concentrated leverage position

“Getting Hwang’d”: a lender - unwinding a margin call - that takes a large loss

Bill Hwang’s family office (started with $200MM in capital, 8yrs ago) took >10% of Credit Suisse & Nomura’s market caps.

[Tbh, that’s an achievement]

For years, Bill Hwang apparently ran leveraged positions in Chinese large-cap tech equities.

That was an all-time-great trade.

And leveraging up a great - multi-year - trade is how you turn $200MM into ~$15BN.

But Bill, like many US Oilmen, found himself with a case of Winner’s Tilt.

He was caught long TMT names - with 4x+ leverage - as they crashed, while short the S&P500 (which is somehow up YTD).

And the following margin-call wiped out the run-of-the-decade, as well as a few bank risk managers in the process -

CREDIT.

OK - here’s where things don’t make sense.

[Bill Hwang’s trade fired up a few thought]

The 10yr is up ~80bps YTD

High growth tech stocks (EM Cloud Index) are down YTD

S&P500 is up YTD

Rising rates should imply that the terminal value component of a DCF declines…

…and yet, the S&P isn’t budging.

[At least credit markets are still being rational]

US IG Corp Credit registered the 2nd largest quarterly loss on record, at -4.4%.

Which is *to be expected* when the 10yr rises.

The credit markets are convinced that interest rates will rise.

And equity markets are convinced that they won’t -

OTHER NEWS.

When oil workers are under siege (Moz)

Suez Canal reopens

Saudi wants to extend cuts

Indonesia refinery fire

The artist fka-Encana sells EF assets

An Equinor discovery

New global solar PV installations to increase 27%

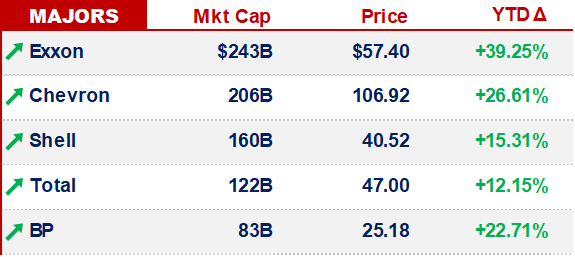

Total / Iraq talk $7BN infrastructure deal

That’s it for this week - catch y’all next Tuesday -