Fortis, S1s & Secondaries

“The meek shall inherit the Earth, but not its mineral rights” - J. Paul Getty

FORTIS.

Fortis - one of EnCap’s minerals business - filed it’s S1 over the weekend.

Long story short, Fortis is STACK + Permian mineral assets:

Currently, most of Fortis’s production is coming from their STACK acreage (see page 8 in the S1) -

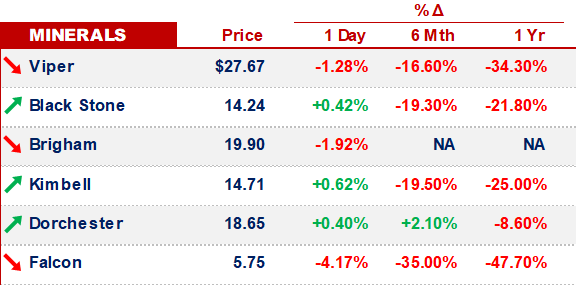

FANG.

Michael Hollis, the President & COO of Diamondback abruptly resigned, for personal reasons. Hollis also resigned from his positions as a director of FANG and Viper Energy Partners -

RBLs.

Ahead of November borrowing base re-determinations, Debtwire is reporting that banks have published price decks, averaging:

$47.33/bbl for 2019 & $48.33/bbl for 2023 for Oil; &

$2.13/MMbtu for 2019 & $2.40/MMbtu for 2023 for Gas

This borrowing base news follows reports of smaller bank lenders reducing and/or selling energy loan book exposure -

SHALE ON THE AIM.

The FT is reporting that US Small Cap E&Ps are increasingly looking to the London Junior Exchange as a serious source of capital raising.

This news follows the recent trend of smaller US-based conventional players listing in London.

Last week, Houston-based Vaalco priced a secondary listing on the AIM, raising capital to fund further acquisitions -

SICHUAN SHALE.

On Sunday, Petrochina announced newly added proven shale gas reserves from the Changning-Weiyuan & Taiyang blocks in the Sichuan basin.

Petrochina also said it had newly proven reserves at the Qingcheng oil field in Ordos basin -

OTHER NEWS.

Harbour Energy’s Chrysaor (backed by EIG) closed the acquisition of Conoco’s North Sea Assets

Total closed the acquisition of Anadarko’s interest in the Mozambique LNG project

That’s it for today - crude/geopolitical news has been relatively calm, for a change - we’ll be back on Friday -