Backtests

“Adapt or perish, now as ever, is nature's inexorable imperative” - H. G. Wells

REGRESSIONS.

About three weeks ago, BAML wrote a quant equity note titled “S&P 500 Relative Value Cheat Sheet”.

[If you haven’t read, we recommend it]

Quant equity strategies apply rules via backtests / regressions, often seeking alpha in statistical patterns (by betting on things like mean-reversion).

OK - now, hold that thought.

With Q3 coming to a close, we found the quarterly winners & losers noteworthy:

*This table does not scream mean-reversion*

For a backtest - or just historical data - to be relevant, historical events have to follow some sort of pattern.

And this year’s obviously an anomaly.

OK - back to the BAML note:

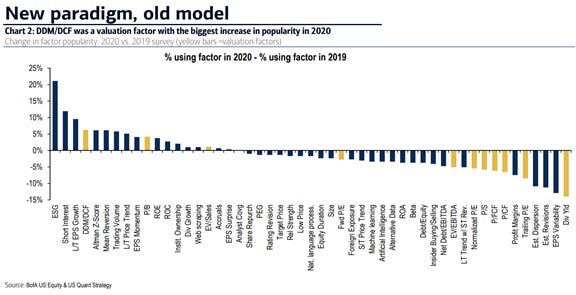

Investors historically have - and have been recently - changed up the factors that they use in their quant equity models.

We suspect that - now - old statistical models are not working in this new world.

On account of historical data being irrelevant.

To us, using these strategies - in times like these - seems crazy.

And - yesterday - we found out that we’re not alone:

Justina Lee’s latest article covering Sanford Bernstein’s top quant’s controversial statements delivered to us what good fiction normally does - the feeling that you’re not alone!

The next step in this story - were we writing it - would be a hard pivot towards using alternative data w/ fundamental valuation models.

Alternative data - whether it be satellite footage of tankers, public / state oil production data, or Google search traffic - is probably the most useful kind of model input, in the context of forecasting in the environment that is 2020.

More specifically, the rate of change of that data -

ARCTIC OIL.

Sweden’s Lundin Energy - perhaps the most successful E&P over the last 5yrs - doubled down on its Arctic exploration program, acquiring interests in a portfolio of licenses in the Barents Sea.

“Lundin on Monday said it would pay Japan’s Idemitsu Kosan $125mm to gain exposure to the Wisting field, which is due to be developed by Norway’s state oil group Equinor by the end of 2022, as well as increase its stake in the smaller Alta field.”

“Alex Schneiter, Lundin’s outgoing chief executive, told the FT in July 2019 that Lundin had 24-36 months to find something in the Norwegian Arctic, otherwise it would face pressure from its board and investors to pull out”

The timing may seem strange, but we’re in no position to critique Lundin.

Long after the North Sea was largely written-off, they (along w/ Equinor) brought online - debatably - the best new field in the last 5yrs.

For that reason alone, we’re taking note of this investment -

KOSMOS.

Kosmos restructured its GoM prepayment facility into a 5yr $200mm term-loan facility, w/ Andy Beal (via CSG) & Trafigura.

Pre-Covid, we thought (a) Kosmos had a comparatively good strategy & (b) that they were (and are still) very good - perhaps the best - at executing it.

That aside, CSG & Trafigura are sharks - sharp ones at that.

We expect this deal will work out well for the lenders.

Hopefully it works out well for Kosmos, too -

OTHER NEWS.

Libya is slowly coming back online

Lenders are taking over bankrupt Sable…

No es bueno

As a counterbalance to our leading thoughts, @Jesse_Livermore wrote a thread that’s worth a read

A surprisingly fun feature of machine learning is that it gives us a more clear window into the past - catch y’all next week -